IMF Urges Tailored Policy Mix Amid Middle East War, AI-Driven Inflation Pressures

In its latest World Economic Outlook, the International Monetary Fund (IMF) warns that the war in the Middle East and the rise of artificial‑intelligence‑driven demand are forcing policymakers to juggle three urgent priorities: containing inflation, sustaining economic activity, and protecting the most vulnerable households.

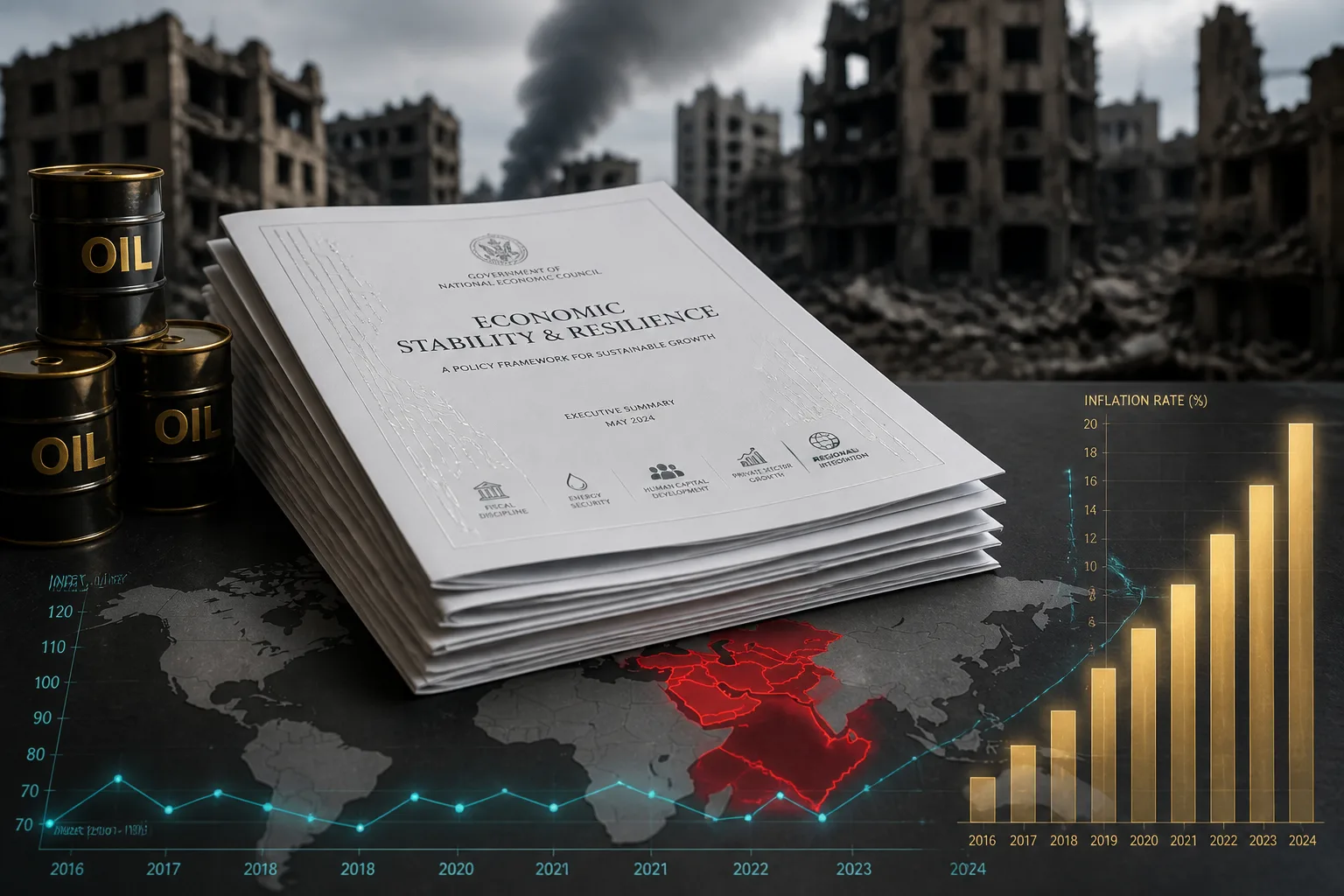

The IMF’s analysis shows that the conflict has amplified commodity price shocks, especially in energy, while AI‑enabled consumption is adding further upward pressure on prices. Together, these forces create a volatile environment in which the financial system faces heightened instability risks.

"Policy makers must address the immediate impact of current shocks while building resilience against future shocks," the IMF says. It stresses that responses must be country‑specific, reflecting differences in inflation dynamics, fiscal space, and financial vulnerabilities, and that international cooperation should be renewed.

Monetary policy, the IMF argues, should remain focused on price stability. Central banks are advised to keep real interest rates steady when inflationary pressures are temporary and expectations are stable, even if nominal rates must rise. When higher inflation coincides with technology‑led demand growth, tighter policy may be required to prevent overheating.

In situations where inflation is already above target at the onset of the war, or where credibility is weaker, the IMF recommends that monetary policy stay tighter for longer or even tighten further to keep expectations in check. Conversely, if a negative demand shock weakens growth and deflates inflation, easing could be considered – but only if it does not compromise the return to price stability.

The IMF highlights communication as a key tool in an uncertain environment. Central banks should clearly explain how new data affects the balance of risks and maintain legal and operational independence to shield policy from political pressures.

Exchange‑rate policy is also emphasized. For inflation‑targeting economies, the IMF recommends that exchange rates remain the primary mechanism to absorb external shocks. However, when currency depreciation threatens inflation or balance‑sheet pressures, temporary foreign‑exchange intervention or targeted capital‑flow management can complement the macro‑policy mix.

Financial‑sector monitoring is another priority. The IMF urges supervisory authorities to intensify risk assessment for sovereign, banking, and non‑bank institutions, ensuring adequate capital, liquidity, and reserve buffers are in place.

Fiscal policy should avoid large‑scale subsidies, tax cuts, and price controls, which are often poorly targeted and costly. Energy‑related fiscal support should be phased out as the shock subsides to preserve fiscal buffers. When support is necessary, it should be temporary, targeted to vulnerable households, and integrated into a broader policy mix that preserves price stability.

Support for companies should be limited to viable, energy‑intensive firms that improve energy efficiency. Any fiscal measures should include clear expiration dates, transparent eligibility criteria, and compensatory mechanisms, especially when fiscal space is limited.

The IMF also cautions that economies benefiting from commodity gains or the global technology cycle should avoid pro‑cyclical spending and instead save or redistribute those gains within a debt‑sustainable framework.

In sum, the IMF’s guidance calls for a coordinated, country‑specific approach that balances immediate relief with long‑term resilience, prioritizes price stability, and safeguards financial stability amid the ongoing Middle East conflict and AI‑driven economic dynamics.

The IMF’s World Economic Outlook, released twice a year, serves as a key reference for policymakers worldwide. Its latest update underscores the complex trade‑offs confronting governments in the region and beyond.